The Memory Super Cycle: Why This Time Is Different

The commodity thesis is dead. Here is why the collision of infinite AI demand and fixed silicon supply is triggering a multi-year repricing of US equities like $SNDK and $MU.

TL;DR: Global semiconductor memory market has shifted from a cyclical commodity to a high-value strategic asset. The primary thesis is that we are entering a multi-year "Memory Super Cycle" driven by a structural supply-demand deficit that cannot be resolved until 2028

Recommended Long Positions in US Equities:

We often hear that “this time is different” is the most dangerous phrase in finance. Usually, it is. It typically precedes a liquidity event that reminds us that gravity, like leverage, works in both directions.

But occasionally, the market undergoes a structural dislocation so profound that historical heuristics fail to capture the new reality. We are currently witnessing such a dislocation in the memory and storage sector. The consensus view treats memory—DRAM and NAND—as a commodity, prone to boom-and-bust cycles dictated by the ruthless math of oversupply. That view is obsolete as of today..

We are currently witnessing a structural break in the supply chain that defies historical precedents. This is not a standard inventory correction; it is a “sovereign” realignment of compute resources. The convergence of GenAI’s voracious appetite for data, a physical limit on fabrication capacity that cannot be resolved before 2028, and a geopolitical imperative to secure domestic supply has created a “perfect storm” for pricing power.

The consensus among market participants is that the price action we are seeing—where Micron Technology MU 0.00%↑ trades near all-time highs and SanDisk SNDK 0.00%↑ guides for explosive growth immediately following its spin-off—is being precipitated by a fundamental shortage of “clean room” space. But it is more than that. It is a signaling mechanism from the Titans of industry. When Mark Liu, the former Chairman of TSMC and a man who arguably understands the physical limits of silicon better than anyone alive, deploys $7.8 million of his own capital into Micron stock at the top of the chart, he is conducting a “rate check” on the entire industry’s skepticism.

We believe that the "Memory Wall" has replaced the "Compute Wall" as the primary constraint on AI scaling. We recommend an aggressive long positioning in SNDK 0.00%↑ and MU 0.00%↑. This thesis is driven by three converging vectors which we will explore in exhaustive detail:

The Concrete Barrier: A physical inability to expand supply due to a lack of greenfield fab readiness until 2028.

The Cannibalization Effect: The hostility of High Bandwidth Memory (HBM) manufacturing to standard wafer yields.

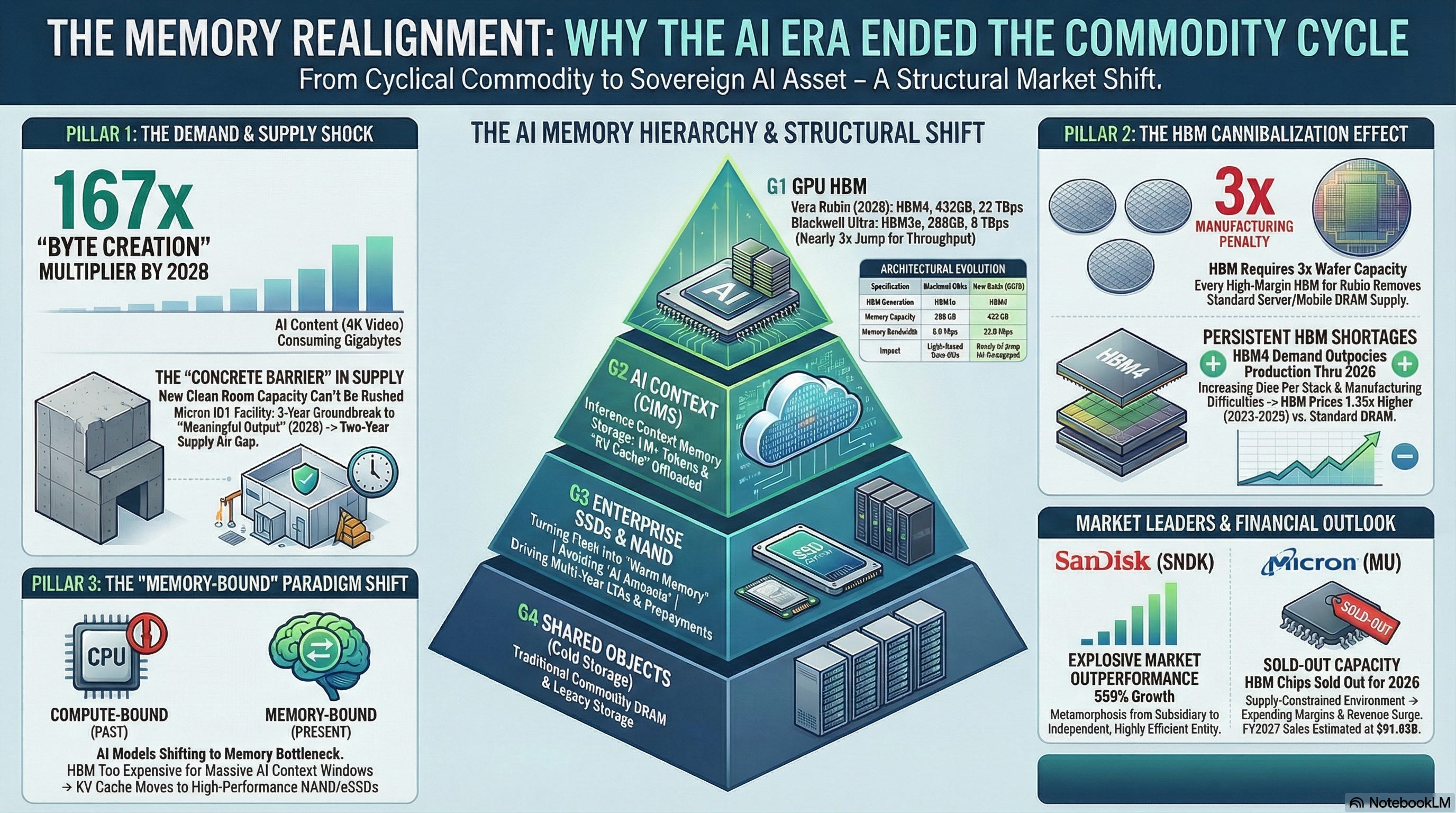

The 167x Multiplier: A transition from human-generated text to AI-generated video that is shattering all existing demand models.

The era of the “one-way” bearish memory trade appears to be ending. The volatility observed this winter is likely just the opening salvo in a protracted adjustment of global compute pricing, ushering in what Asian market analysts are already calling the “Year of the Fire Horse”—a time of rapid, volatile, and unstoppable acceleration.

The Macro-Geopolitical Context

The “Treasury Put” for Silicon

To understand the magnitude of the current opportunity in US memory equities, one must first discard the traditional “cyclical” framework that has governed the sector since the dot-com bust. Historically, memory was a play on PC and smartphone unit volumes. When consumers bought more laptops, Micron sold more DRAM. When the cycle turned, prices collapsed, and investors fled.

That dynamic relied on a free-market global supply chain where capital could flow efficiently to the lowest-cost producer (often in Asia) to bring new supply online. That world no longer exists.

The current administration, much like the one described in the “Mar-a-Lago” thesis , has made re-industrialization a cornerstone of its economic platform. The “Chips and Science Act” was not merely a subsidy program; it was a signal that the US government views domestic memory production as a national security imperative. In this new regime, the “Fed Put”—the central bank’s implicit guarantee to support asset prices—has been replaced by a “Treasury Put” for the manufacturing sector.

The United States cannot afford for US AI infrastrcture suppliers to fail, nor can it afford for the AI revolution to stall due to a lack of storage. This geopolitical floor fundamentally alters the risk premium for US-domiciled memory producers. It suggests that the “boom-bust” cycles of the past will be smoothed by state-sponsored demand and protectionist pricing power.

The “Rate Check” in the Physical Market

In the currency markets, a “rate check” is a signaling mechanism where a central bank asks dealers for prices to imply that intervention is imminent. In the semiconductor market, we are seeing a similar phenomenon, but the actors are not central bankers; they are the hyperscalers (Microsoft, Meta, Google) and the hardware architects (Nvidia).

Jensen Huang’s comments at CES 2026 served as a massive “rate check” on the storage industry. By declaring storage “a completely unserved market” , he signaled to every data center architect in the world that their current infrastructure was obsolete. This was not a suggestion; it was a directive. The “dealers” (in this case, the procurement officers at major cloud providers) immediately adjusted their positioning. They stopped buying on the spot market and started signing Multi-Year Long-Term Agreements (LTAs) with prepayments.

This shift in expectations—from “just-in-time” inventory management to “strategic hoarding”—is what triggered the sudden tightening in the market. Just as the Yen weakened when the Bank of Japan signaled tolerance for inflation, the availability of high-performance NAND and DRAM has evaporated as the market signaled a tolerance for higher prices to secure supply.

The “Fire Horse” Anomaly

The year 2026 corresponds to the “Year of the Fire Horse” in the Chinese zodiac. Historically, this sign is associated with volatility, rapid change, and irrepressible energy. In Japanese culture, it is viewed with superstition; in the markets, it is viewed as a time of disruption.

Bernstein analysts have latched onto this metaphor to describe the current setup for SanDisk. The “Fire Horse” guide implies a market environment that breaks the statistical norms. We are seeing standard deviation moves in pricing—blended DDR contract prices rising 62% in a single quarter —that are statistically improbable without an external shock.

This report will demonstrate that the shock is not external, but internal. It is the result of a decade of underinvestment colliding with the greatest demand shock in the history of computing.

Reason #1: The Demand/Supply Dislocation

1. The Concrete Barrier: Why We Cannot Build Our Way Out

The first and most durable reason for this shortage is physical. It is rooted in the construction schedules of the American West and the clean room requirements of the Angstrom era.

The “Ghost” Fabs of 2026

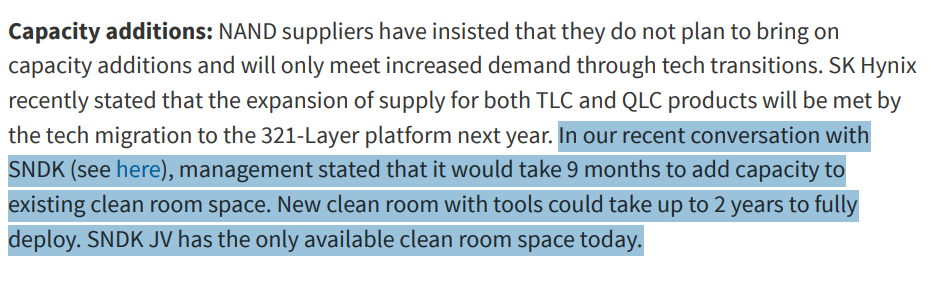

In previous cycles, when memory prices spiked, Samsung, SK Hynix, and Micron would simply accelerate their equipment orders. The buildings—the massive, windowless shells that house the fabs—were usually built years in advance, sitting empty as “warm shells” waiting for tools.

This time, the shells are full. The industry, burned by the inventory corrections of 2022 and 2023, halted new construction. They practiced “disciplined capex,” a euphemism for starving the supply chain to restore profitability.

Now that demand has returned with a vengeance, the industry finds itself hitting a “Concrete Barrier.” Micron’s VP of Marketing, Christopher Moore, was explicit in his assessment: “In order to dramatically increase the number of bits, we need more clean room space. And that takes a lot of time”.

The timeline he laid out is sobering for anyone expecting a quick fix:

Groundbreaking: Micron broke ground on its massive ID1 facility in Boise, Idaho, three years ago.

Completion: The facility is not expected to come online until mid-2027.

Production: Even after the building is finished, the complex process of qualifying tools and ramping yield means that “meaningful output” will not hit the market until 2028.

This creates a two-year supply air gap. From early 2026 through the end of 2027, there is essentially zero net new greenfield capacity entering the global market that can move the needle on supply. The “supply response” that economists rely on to balance markets is physically impossible. You cannot cheat the cure time of concrete, nor can you rush the installation of extreme ultraviolet (EUV) lithography scanners, which are themselves in short supply.

The Clean Room Crisis

It is not just about the size of the building; it is about the quality of the air inside. The transition to advanced nodes (1-beta and 1-gamma for DRAM, 200+ layer for NAND) requires Class 1 clean rooms of unprecedented purity.

As Lam Research CEO Tim Archer noted, the growth in wafer fab equipment spending is “constrained by a shortage of available clean room space”. This is a vicious feedback loop: the equipment makers (Applied Materials, Lam) are seeing record orders, but they cannot ship the tools because the customers (Micron, Samsung) have nowhere to put them.

This physical constraint acts as a hard ceiling on supply. No matter how high the price of HBM goes, and no matter how desperate Nvidia becomes for memory, the industry cannot conjure clean room space out of thin air. This ensures that the shortage will remain structural, rather than cyclical, for at least the next eight quarters.

2. The GenAI Data Growth Shock

While supply is constrained by physics, demand is being unconstrained by algorithms.

The growth of Generative AI has moved beyond the “training” phase and into the “inference” and “agentic” phases. This shift has profound implications for memory consumption.

The “Training” vs. “Inference” Fallacy

For the past two years, the market focused on the memory required to train models like GPT-4. This was a massive, but discrete, demand pulse. We are now entering the era of inference—the actual use of these models by billions of users and autonomous agents.

UBS estimates that AI demand is now “well over memory supply” and will remain so into 2027. The demand profile has shifted from a “bursty” training workload to a sustained, high-bandwidth inference workload that runs 24/7.

The Server Refresh Super Cycle

Data centers are in the midst of a massive refresh cycle to accommodate these new workloads. Standard servers are being ripped out and replaced with AI-ready racks.

Server Unit Growth: Forecast to grow +13% YoY in 2026.

Content Per Box: This is the multiplier. The average AI server requires significantly more DRAM and NAND than a traditional CPU server. UBS forecasts server DDR bit demand to grow +46% YoY in 2026, accounting for 34% of the total DRAM market.

This is not a linear increase; it is a step-function change. The “content per box” is exploding because the CPUs (like AMD’s EPYC and Intel’s Xeon) are expanding their core counts to keep up with the GPUs, and each core requires more memory bandwidth and capacity to function efficiently.

3. The Supply/Demand Deficit

When we overlay the “Concrete Barrier” (flat supply) against the “GenAI Shock” (exponential demand), the result is a deficit of historic proportions.

UBS forecasts the DRAM industry to remain undersupplied until 4Q27, a significant extension from previous estimates. The NAND market, often considered the “looser” of the two, is now expected to remain in deficit until 1Q27.

This is the “impossible policy dilemma” for the buyers. They know supply is fixed. They know their own demand is growing. Their only option is to panic-buy, which drives the very price spiraling they seek to avoid. This psychological shift—from managing inventory to securing survival—is what drives the “Fire Horse” cycle.

Reason #2: The Technical Drivers of the Shortage

Beyond the simple “lack of fabs,” there are two highly technical, structural reasons why this shortage is unique. The first of these is the Cannibalization Effect of High Bandwidth Memory (HBM).

The Physics of HBM Cannibalization

To the layman, “memory is memory.” A silicon wafer goes in, and chips come out. But in the era of AI, not all chips are created equal, and the production of one type actively destroys the capacity for another.

High Bandwidth Memory (HBM), specifically the HBM3E and upcoming HBM4 generations used by Nvidia, is an incredibly inefficient product to manufacture in terms of wafer usage.

Die Size Penalty: HBM dies are larger than standard DDR dies to accommodate the Through-Silicon Vias (TSVs) required for stacking.

Yield Penalty: Stacking 8 or 12 dies vertically means that a single defect in any one of the layers can render the entire stack unusable (though repair techniques exist, the yield loss is still significant).

Wafer Consumption: Manufacturing 1 GB of HBM requires approximately 3x the wafer capacity of manufacturing 1 GB of standard DDR5.

This is the “Cannibalization Effect.” Every wafer that Micron or SK Hynix allocates to HBM—which they must do to satisfy Nvidia and capture the massive price premium—is a wafer that cannot be used to make standard server DRAM or mobile LPDDR.

“Eating” the Capacity

UBS describes this explicitly: increased HBM forecasts “continue to ‘eat away’ DDR capacity”. The industry is not expanding total wafer starts (due to the Concrete Barrier); it is merely shifting the mix.

As more capacity is diverted to the high-margin “AI Lane” (HBM), the “Commodity Lane” (DDR5/NAND) is left starved. This creates a shortage in the standard memory market that is entirely artificial, driven by the displacement of wafers.

This explains why we are seeing such violent price moves in standard DDR.

Blended DDR Pricing: Forecast to increase +62% QoQ in 1Q26.

Server DDR5 Quotes: Some quotes are up over +70%.

This is the “rate check” playing out in the physical market. The price of the commodity is skyrocketing because the factory is busy building the luxury good. The “supply” of DDR5 is effectively shrinking even as demand grows, squeezed out by the insatiable need for HBM.

The Equipment Bottleneck

This cannibalization extends to the tools themselves. The clean room space that is available is being filled with the specialized bonding and metrology tools needed for HBM stacking, rather than the high-throughput lithography tools needed for volume DDR production.

Applied Materials and Lam Research are beneficiaries of this , but for the memory buyers, it is a disaster. The industry has effectively capped its own ability to produce standard memory for the next two years in a desperate bid to chase the AI gold rush.

Reason #3: The “Byte Creation” Multiplier

The second technical driver—and perhaps the most profound—is a change in the nature of the data itself. We are moving from the “Text Era” to the “Video Era” of AI, and the implications for storage (NAND) are catastrophic for the short sellers.

The 167x Growth Vector

For the last decade, “Big Data” was dominated by logs, transactions, and text. Text is highly compressible. A billion words of text takes up negligible space on a modern SSD.

Generative AI is changing this. The new frontier is text-to-video and multimodal generation.

The Multiplier: According to Seagate, by 2028, the creation of image and video content by AI models is projected to grow 167 times.

Data Density: A single minute of AI-generated 4K video consumes gigabytes of storage. When millions of users begin generating video content daily—for entertainment, marketing, or communication—the “byte creation” rate of humanity will undergo a hyper-inflationary event.

This is what SanDisk management refers to when they speak of a “structural evolution” where NAND becomes indispensable. The world is about to drown in synthetic media, and all of that media must be stored.

The “Context Memory” Crisis

It is not just about storing the output; it is about the “working memory” of the AI itself.

As AI models evolve into “Agents” that run autonomously for days or weeks, they need to maintain a “context”—a history of everything they have seen, done, and planned.

The Memory Wall: Storing this context in HBM is too expensive (at $100+ per GB) and capacity-constrained.

The Solution: Nvidia is pushing a new architecture where this context is offloaded to high-performance Enterprise SSDs (eSSDs).

This effectively turns SanDisk’s NAND Flash into a tier of “slow RAM.” It blurs the line between storage and memory.

The Impact: SanDisk estimates that this “Key-Value (KV) Cache” demand—which is not currently in the baseline forecasts—could add 75-100 Exabytes (EB) of demand in 2027 alone.

Double Down: This incremental demand could double again in 2028.

To put this in perspective, 100 Exabytes is massive. It represents a “hidden” layer of demand that the market has not priced in. This is the “Reason #3” that makes this shortage unique: we are creating a new category of memory usage that never existed before.

The Anecdote: Anecdotal Evidence – The Signals from the Top

The statistical data is compelling, but in financial markets, the “anecdote” often leads the “data.” Two specific events in early 2026 serve as the “smoking gun” for this thesis.

Jensen Huang’s “Unserved Market” Declaration

At CES 2026, Nvidia CEO Jensen Huang did not just launch a chip; he indicted the entire storage industry.

While unveiling the “Vera Rubin” platform, Huang made a comment that sent shockwaves through the technical community: he described storage as “a completely unserved market today”.

This phrasing is deliberate. Huang does not mince words. By calling the market “unserved,” he is stating that the current generation of storage products (HDD and standard SSD) is incapable of meeting the I/O requirements of the Rubin architecture.

He elaborated: “The amount of context memory, the amount of token memory that we process... is now just way too high. You’re not going to keep up with the old storage system”.

This was a public “Capital Call” to the memory industry. It was Nvidia telling Micron and SanDisk that they need to step up, or the AI revolution will hit a wall. It validates the “Context Memory” thesis (Reason #3) and confirms that the demand for high-performance storage is not a projection, but an engineering necessity for the next generation of GPUs.

Mark Liu’s $7.8 Million Wager

If Jensen Huang provided the technical signal, Mark Liu provided the financial signal.

Mark Liu is not a typical corporate director. He is the former Chairman of TSMC (Taiwan Semiconductor Manufacturing Company). He ran the company that manufactures virtually all of the world’s advanced AI chips. He knows the wafer supply chain down to the atomic level.

In January 2026, just as Micron stock was trading near its all-time highs ($336-$337), Mark Liu executed a series of open-market purchases totaling $7.8 million.

The Signal: Corporate insiders typically buy when their stock is beaten down (”buying the dip”). They rarely buy at the absolute peak (”buying the breakout”).

The Implication: For a semiconductor veteran of Liu’s caliber to buy Micron at an all-time high suggests he sees something the market does not. He sees the “Concrete Barrier.” He sees the “Cannibalization.” He sees the “Order Book.”

His purchase is a “vote of confidence” in the durability of the cycle. It suggests that what looks like a “peak” to a technical analyst looks like the “foothills” to an industry insider. It is the ultimate insider validation of the “Super Cycle” thesis.

The Equity Recommendations

Given this backdrop—a physical shortage, a technical cannibalization, a demand multiplier, and massive insider confidence—how should investors position themselves?

We recommend a concentrated “barbell” trade: SanDisk (SNDK) for the pure-play storage explosion, and Micron Technology (MU) for the strategic HBM dominance.

SanDisk (SNDK): The “Fire Horse” Alpha

The Setup:

SanDisk recently completed its spin-off from Western Digital, becoming an independent, pure-play flash memory company. Spin-offs often create “orphaned” securities that are mispriced by the market, creating a window of opportunity for astute investors.

The Thesis:

Explosive Data Center Growth: SanDisk is successfully pivoting its mix toward the high-margin Data Center market. In FQ2’26, Data Center revenue exploded +64% QoQ and +76% YoY.

The “Fire Horse” Guide: Bernstein analysts have raised their price target to $1,000, citing the “Year of the Fire Horse” as a period of exceptional growth. They argue that the market is underestimating the company’s earnings power as it shifts to long-term agreements.

Valuation Dislocation: Despite the massive growth, the stock trades at a dynamic PE of ~10-11x based on annualized earnings potential ($8B+ annualized net profit). This is a “value” multiple on a “hyper-growth” asset.

Structural Shift: SanDisk is leading the charge in shifting customers to Multi-Year Long-Term Agreements (LTAs) with prepayments. This transforms the business from a volatile commodity seller to a predictable infrastructure provider, warranting a higher valuation multiple.

Recommendation: Buy SNDK as the primary vehicle for the “167x Byte Creation” thesis.

Micron Technology (MU): The Strategic “Arms Dealer”

The Setup:

Micron is the only US-based manufacturer of memory. In a world of fragmenting geopolitical blocs (as hinted at in the “Mar-a-Lago” intro), Micron is a strategic national asset.

The Thesis:

HBM Leadership: Micron’s HBM3E is sold out for 2025 and much of 2026. They are successfully ramping yield and taking share from competitors.

Pricing Power: As the HBM cannibalization effect drives up standard DDR prices (+62% QoQ), Micron’s legacy business becomes a cash cow.

The “Treasury Put”: The US government’s support for domestic fabs (via the CHIPS Act and other vehicles) provides a floor for Micron’s capital expenditure, de-risking the “Concrete Barrier” build-out.

Insider Conviction: Mark Liu’s purchase is the cherry on top. If the former head of TSMC is betting $7.8 million on MU at these levels, we should follow.

Recommendation: Buy MU as the “picks and shovels” play for the AI compute infrastructure.

IMPORTANT DISCLOSURES

Not Financial Advice: This report is strictly for informational and educational purposes and should not be considered financial, investment, legal, or tax advice. While the information presented here is believed to be reliable, we make no representations or warranties regarding its accuracy or completeness. This content is not a recommendation, solicitation, or offer to buy or sell any securities. Please conduct your own due diligence and consult with a qualified advisor before making investment decisions. Note that the author may hold vested interests in the securities mentioned.